The Imperative of Timely ROC Annual Compliance for FY 2025-26

For every company registered under the Companies Act, 2013, annual compliance with the Registrar of Companies (ROC) is not merely a formality; it is a statutory obligation that dictates the company’s legal standing. As we approach the filing season for the Financial Year (FY) 2025-26, understanding the precise deadlines is paramount. Missing the crucial AOC-4 MGT-7 filing due date 2026 can lead to steep financial penalties and severe consequences, including the disqualification of directors.

This comprehensive guide is designed to navigate the complexities of ROC annual filing, providing clarity on the specific forms, deadlines, and the punitive measures enforced by the Ministry of Corporate Affairs (MCA). Staying ahead of the curve ensures your business maintains its ‘Active’ status and avoids costly regulatory setbacks.

Decoding the Mandatory Annual ROC Filings and the AOC-4 MGT-7 Filing Due Date 2026

Annual filing primarily revolves around two critical e-forms: AOC-4 (for financial statements) and MGT-7 or MGT-7A (for the annual return). The requirements vary slightly depending on the company type (Private Limited, Public Limited, One Person Company, etc.), but the core obligation remains universal.

Form AOC-4: Reporting Financial Statements

Form AOC-4 is the official mechanism for filing the company’s financial statements and supporting documents with the ROC. This includes the Balance Sheet, Profit & Loss Account, Director’s Report, and Auditor’s Report.

- Applicability: Mandatory for all companies.

- Due Date Principle: Must be filed within 30 days of the company’s Annual General Meeting (AGM).

- Key Requirement: Requires certification by a practicing professional (CA/CS/CWA) if the paid-up capital exceeds a certain threshold or if specific compliance requirements apply.

Form MGT-7/MGT-7A: The Annual Return

MGT-7 is the comprehensive annual return form detailing the company’s structure, management, indebtedness, shareholding pattern, and changes in directorship over the financial year. For smaller companies (like One Person Companies or small companies), a simplified form, MGT-7A, is used.

- Applicability: MGT-7 for most companies; MGT-7A for small companies and OPCs.

- Due Date Principle: Must be filed within 60 days of the company’s Annual General Meeting (AGM).

- Key Requirement: Requires certification by a practicing Company Secretary (CS) if the company’s paid-up share capital is Rs. 10 crore or more, or turnover is Rs. 50 crore or more.

The Critical AOC-4 MGT-7 Filing Due Date 2026 Compliance Calendar

The calculation of the AOC-4 MGT-7 filing due date 2026 hinges entirely on the date the company conducts its Annual General Meeting (AGM). For the financial year ending March 31, 2026 (FY 2025-26), the AGM must generally be held within six months of the financial year end, which is September 30, 2026.

Assuming a company holds its AGM on the statutory deadline of September 30, 2026, the corresponding ROC filing deadlines would be:

Mandatory AGM Deadline (FY 2025-26)

The AGM must be concluded by September 30, 2026. This is the pivotal date that sets the clock running for both AOC-4 and MGT-7 filings.

AOC-4 Due Date (30 Days Post-AGM)

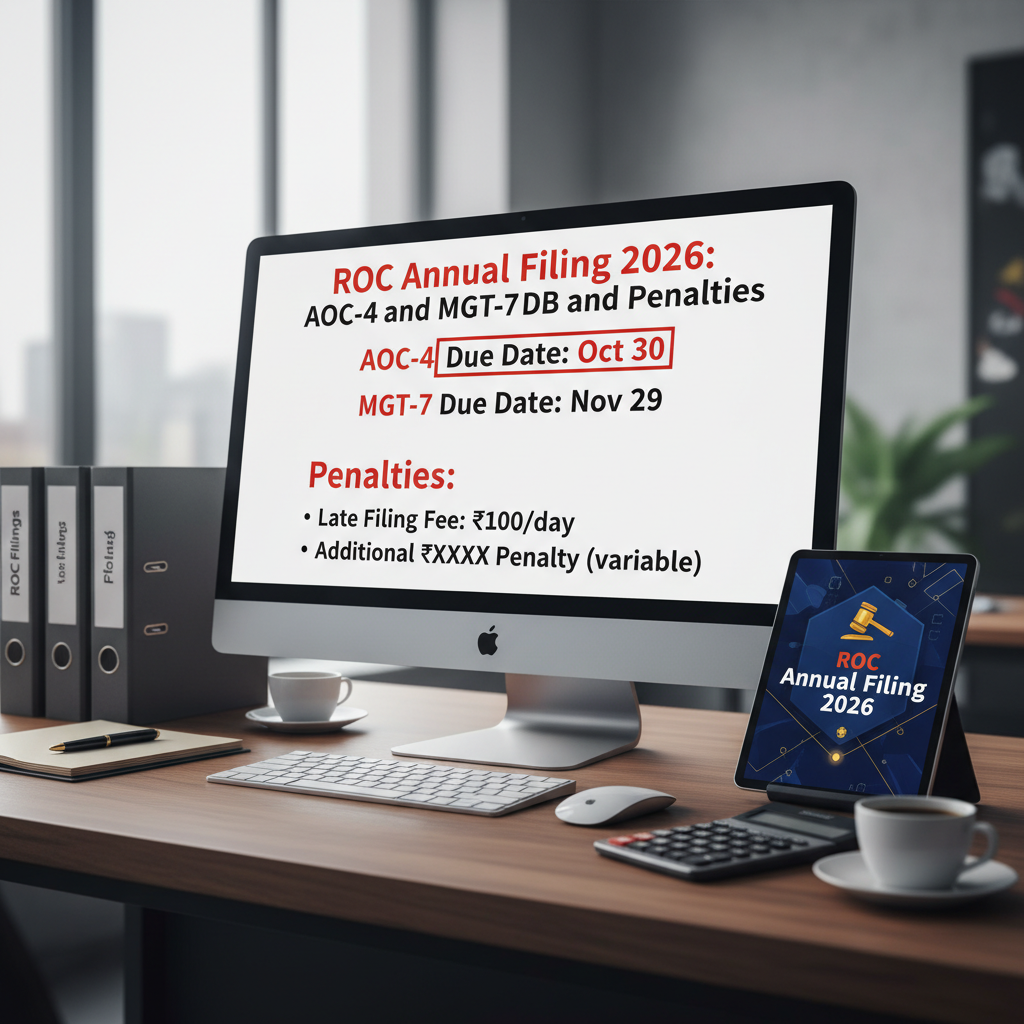

If the AGM is held on September 30, 2026, the deadline for filing Form AOC-4 is October 30, 2026.

MGT-7/7A Due Date (60 Days Post-AGM)

If the AGM is held on September 30, 2026, the deadline for filing Form MGT-7 or MGT-7A is November 29, 2026.

Understanding the AGM Requirement and Timeline

It is crucial to note that the AGM must be held first. If the company is unable to hold its AGM by September 30, 2026, it must apply for an extension from the ROC (if eligible). However, the filing deadlines for AOC-4 and MGT-7 are still calculated from the actual date the AGM was held, or the extended due date granted by the ROC.

“Compliance is about discipline, not just deadlines. A disciplined approach ensures that the financial data is ready and audited well before the statutory filing window opens,” notes corporate law experts.

Navigating the Penalties and Late Fees for Missing the AOC-4 MGT-7 Filing Due Date 2026

The penalties for failing to adhere to the AOC-4 MGT-7 filing due date 2026 have become significantly harsher under the Companies Act, 2013, compared to previous regimes. The current penalties are designed to discourage default strictly.

The Per Day Fine Structure

If a company misses the statutory deadline, it must pay an additional fee (late fee) calculated from the day immediately following the due date until the actual date of filing. This fee is non-negotiable and accumulates rapidly.

Standard Late Fee Rate

The primary penalty for late filing of both AOC-4 and MGT-7 is Rs. 100 per day of delay for each form, in addition to the normal filing fee.

Impact on Company Status

Chronic non-compliance can lead to the company being marked as ‘Inactive’ or, in severe cases, the ROC initiating the process of striking off the company’s name from the register.

Director Disqualification Risk

If a company fails to file its annual returns and financial statements for a continuous period of three financial years, the directors of that company risk disqualification for five years.

The financial burden of late filing can quickly escalate. For example, delaying both forms by just 60 days means incurring Rs. 6,000 in penalties (Rs. 3,000 for AOC-4 + Rs. 3,000 for MGT-7), excluding the base filing fees. This is a crucial area where proactive planning saves significant resources. You can review the official fee structure updates directly on the Ministry of Corporate Affairs (MCA) website to ensure accuracy.

Strategies to Ensure Timely AOC-4 MGT-7 Filing Due Date 2026 Compliance

Avoiding penalties requires a robust internal compliance mechanism and proactive engagement with auditors and professionals. Here are actionable steps companies can take:

- Pre-Audit Preparation: Ensure all books of accounts are finalized, bank reconciliations are complete, and necessary supporting documents (like invoices, vouchers, and statutory registers) are organized well before the financial year ends.

- Statutory Registers Update: Regularly update statutory registers (Register of Directors, Register of Members, etc.). These details form the basis of Form MGT-7, and discrepancies cause significant delays during filing. For newly established entities, foundational compliance is key, as detailed in guides like the incorporation of a private company guide.

- Early AGM Scheduling: Do not wait until September 30th. Schedule the AGM in August or early September 2026. An earlier AGM provides a buffer period to address any technical glitches or discrepancies discovered during the final review of the e-forms.

- Professional Consultation: Engage experienced professionals for certification and filing. Expertise minimizes errors that could lead to resubmission and further delay. If you require expert guidance throughout the year, reliable assistance can be found through comprehensive Company Compliance Services.

Digital Filing Requirements and E-Forms Checklist

The entire ROC filing process is digital, utilizing the MCA V3 portal. Companies must ensure they have all prerequisites in place before attempting the submission. A small oversight in documentation can halt the entire process.

Essential Documentation Checklist for AOC-4 and MGT-7

AOC-4 Attachments

- Audited Financial Statements (Balance Sheet & P&L)

- Board’s Report and Auditor’s Report

- Statement of Subsidiaries (if applicable)

- Details of CSR spending (if applicable)

MGT-7/7A Prerequisites

- List of Shareholders and Debenture Holders

- Details of Directors and Key Managerial Personnel (KMP)

- Details of meetings of Members/Board/Committees

- Shareholding pattern changes during the year

Technical Requirements

- Valid Director Identification Numbers (DINs)

- Updated Digital Signature Certificates (DSCs) of directors and certifying professionals

- Active Status of the company on the MCA portal

It is worth emphasizing the importance of accurate data representation. Any misstatement in the annual filing documents can attract scrutiny and potential prosecution under Section 448 (Punishment for false statement) of the Companies Act, 2013. Therefore, meticulous preparation and cross-verification are non-negotiable steps in the compliance journey. For a deeper understanding of corporate governance requirements, resources detailing the regulatory environment are highly recommended, such as those provided by the Institute of Company Secretaries of India (ICSI).

The Importance of XBRL Filing (AOC-4 XBRL)

Certain classes of companies are mandated to file their financial statements using the Extensible Business Reporting Language (XBRL) format, which involves filing Form AOC-4 XBRL instead of the standard AOC-4. This requirement typically applies to listed companies, companies with a paid-up capital of Rs. 5 crore or more, or those with a turnover of Rs. 100 crore or more.

If your company falls under these categories, the complexity of compliance increases, requiring specialized software and expertise to map financial data correctly into the XBRL taxonomy. Failure to file in the correct format is treated as a default, attracting the same penalties as late filing. Ensuring your compliance team understands this distinction is vital to meeting the AOC-4 MGT-7 filing due date 2026 successfully.

Conclusion: Making the AOC-4 MGT-7 Filing Due Date 2026 a Priority

The annual filing cycle for FY 2025-26, culminating in the crucial AOC-4 MGT-7 filing due date 2026, demands proactive management. The penalties—Rs. 100 per day per form—are steep, but the risk of director disqualification poses an even greater threat to the stability and reputation of the company. By prioritizing the finalization of accounts, scheduling the AGM early, and ensuring the validity of all digital documentation, companies can seamlessly navigate the compliance requirements and maintain a strong legal footing with the Registrar of Companies.

FAQs

The deadlines are dependent on the date of the Annual General Meeting (AGM). Assuming the AGM is held on the statutory deadline of September 30, 2026, the AOC-4 due date is October 30, 2026 (30 days post-AGM), and the MGT-7/7A due date is November 29, 2026 (60 days post-AGM).

The penalty for late filing is currently Rs. 100 per day of delay for each form (AOC-4 and MGT-7), in addition to the standard government filing fee. This penalty accrues daily until the date of actual submission.

No. The filing sequence is mandatory. The financial statements (AOC-4) must be approved and adopted in the AGM first. MGT-7 (Annual Return) contains data derived from the financial statements and the AGM proceedings, meaning AOC-4 must be filed before or concurrent with MGT-7, but usually, it is filed first.

Failure to file annual returns (MGT-7) and financial statements (AOC-4) for three consecutive financial years can lead to the company being declared ‘Inactive’ and can result in the disqualification of all directors associated with the company for a period of five years.

Yes, OPCs are required to file annual returns, but they file a simplified version of the forms. They file AOC-4 and MGT-7A (instead of MGT-7). The deadline calculation is slightly different as OPCs do not need to hold an AGM; they must file within 180 days from the close of the financial year (September 27, 2026).